Stock buybacks, explained

The tax cuts have put stock buybacks in the spotlight. Here’s what they are — and why you should care.

The Republican tax cuts have been great for corporations, which have spent billions of the dollars they’ve reaped in savings buying up their own stock to reward shareholders and investors. Corporate executives and insiders are taking advantage of the stock buyback boom to sell shares they own to the companies they work for, profiting handsomely. Companies are spending millions and billions

There’s nothing illegal about any of it, at least not in the United States.

The $1.5 trillion GOP tax cuts, which slashed the corporate tax rate to 21 percent from 35 percent and reduced the rate on corporate income brought back from abroad, have been a major boon to corporate America. They’ve also put the spotlight on stock buybacks, which have been on the rise for years and are on track to reach $800 billion in 2018.

In a stock buyback, a company repurchases its own shares from the broader marketplace, usually through the open market. That leaves the remaining shareholders with a bigger chunk of the company and increases the earnings they reap per share, on top of the regular dividend payments that companies make to shareholders out of their profits.

From 2007 through 2016, S&P 500 companies distributed $4.2 trillion to shareholders through stock buybacks and an additional $2.8 trillion through dividends, totaling $7 trillion in shareholder payouts. From 2003 through 2012, S&P companies used 54 percent of their total earnings — $2.4 trillion — to buy back stock.

Stock buybacks and dividends aren’t necessarily a bad thing — they’re a way for shareholders to reap the rewards of a company’s success. But shareholder primacy , in which corporate boards prioritize maximizing profits and returns to shareholders above all else, has been on the rise since the 1980s — along with a focus on short-term profits instead of long-term stability and success.

The concern is that companies, especially in prioritizing buybacks, are rewarding stockholders instead of investing in their workers, research and development, new facilities, or other more productive arenas. Firms also sometimes use buybacks to prop up their stock prices, and corporate executives reap the financial rewards.

A 1982 SEC rule under Reagan opened the stock buyback floodgates

After the stock market crash of 1929 and the Great Depression, the United States government passed the Securities Act of 1933 and the Securities Exchange Act of 1934 to try to prevent it from happening again. The 1934 legislation didn’t bar stock buybacks, per se, but it barred companies from doing anything to manipulate their stock prices. Companies knew that if they did a stock buyback, it could open them up to being accused by the Securities and Exchange Commission of having tried to manipulate their stock price, so most just didn’t.

“It wasn’t illegal, but they were open to liability,” Lenore Palladino, a senior economist and policy counsel at think tank the Roosevelt Institute, told me.

In the 1960s and 1970s, ideas about changing the laws around stock buybacks began to bubble up, and the SEC began to consider moderate rule changes that would make them easier to conduct. But they were not adopted until Ronald Reagan took the presidency.

Reagan appointed John Shad to head the SEC in 1981. A former vice chair of a major Wall Street securities firm, Shad was the first financial executive to head the agency in 50 years, and it showed. In 1982, the SEC adopted rule 10b-18 , which provides a “safe harbor” for companies in stock buybacks. As long as companies stick to specific parameters — such as not buying more than 25 percent of the stock’s average daily trading volume in a single day — they won’t be dinged for stock manipulation.

William Lazonick, an economics professor at the University of Massachusetts Lowell whose Harvard Business Review paper Profits Without Prosperity has influenced thinking on stock buybacks, said Shad’s appointment to the SEC and the accompanying changes, including rule 10b-18, brought about a shift at the agency that continues today.

“Everything they did from that point forward … was turning the SEC from a regulator of the stock market to a promoter of the stock market,” he said.

Lazonick also put the 25 percent average daily trading volume limit into perspective: Apple, which just announced a $100 billion stock buyback , could spend about $1.4 billion per day on buybacks. Microsoft could spend $500 million, and ExxonMobil $200 million.

Stock buybacks have been booming

Companies have spent trillions of dollars on their shareholders since the 1980s. Over the last 15 years, firms have spent an estimated 94 percent of corporate profits on buybacks and dividends.

Beyond the SEC’s 1982 rule that provided a safe harbor for buybacks, shareholder primacy on Wall Street has been on the rise. So-called “ activist investors ” who buy large numbers of a company’s shares to try to get seats on the board or effect change within the company have contributed to a rise in “short-termism” on Wall Street.

They’re names you’ve probably heard of — billionaire hedge fund managers and big-name investors such as Paul Singer, Carl Icahn, and Bill Ackman. Icahn, for example, undertook a major public campaign to get Apple to increase stock buybacks after buying into the company in 2013. When he got what he want out of it, he cashed out less than three years later, and made some $2 billion in the process .

Companies have also found that it’s easy to invest in share buybacks, and it’s a decision Wall Street tends to reward.

“If you’re a corporate manager and you’ve got cash on the books and you’ve got investors looking for you to return it, doing a buyback is easy. It’s a decision that will be popular, that will be cheap, that our rules make easy. And it requires no research and development, no investment in communities, no long-term strategic thinking,” SEC Commissioner Robert Jackson said. “Sometimes the easy thing is also the right thing, but a lot of the times it’s not.”

The thing is, when companies are investing in stock buybacks and dividends, they’re spending money they could use on something else.

The Roosevelt Institute in May released a report estimating that Walmart , for example, could boost hourly wages to over $15 an hour with the $20 billion it was using for a buyback. A separate study from the Roosevelt Institute released in July found that companies spent nearly 60 percent of net profits on buybacks from 2014 to 2017. It estimated that with the money allocated to buybacks, companies such as Lowes, CVS, and Home Depot could give each of their workers a raise of at least $18,000 a year.

Harley-Davidson in February announced a nearly $700 million stock buyback plan just days after saying it would close a plant in Kansas City. Wells Fargo is spending $25 billion on buybacks and is at the same time laying off workers in multiple states .

Lazonick pointed to the pharmaceutical industry as another example of an area where stock buybacks are affecting investment. He researched 19 pharmaceutical companies in the S&P 500, including Johnson & Johnson, Pfizer, and Merck, from 2007 to 2016 and found that they spent more than 90 percent of their net income during that period on buybacks and dividends.

“A lot of it has been due to the fact that they can get away with it,” Palladino, from the Roosevelt Institute, said.

In 2014, Larry Fink, the CEO of BlackRock, one of the largest investment companies in the world, warned US companies to slow it down on buybacks and dividends. “We certainly believe that returning cash to shareholders should be part of a balanced capital strategy; however, when done for the wrong reasons and at the expense of capital investment, it can jeopardize a company’s ability to generate sustainable long-term returns,” he wrote in a letter.

There are some points in favor of a stock buyback. Proponents note that the moves are putting money back into the economy, and they lead to a rise in stock prices, which can have a marginally positive effect on consumer confidence and consumption. And maybe a company’s shares really are cheap, and the company has nothing better to do with its money to buy back stock. But, of course, how often that’s the case is questionable.

The tax cuts are making it worse, and the SEC isn’t helping

Tax cuts have exacerbated shareholder rewards on Wall Street. JP Morgan estimates that S&P 500 companies will buy back a record $800 billion of their own shares this year, thanks in large part to tax savings, strong earnings, and repatriation of profits they previously kept overseas.

“The folks who passed this tax cut did so understanding that it was going to lead this result,” Jackson, the SEC commissioner, told me.

Stock buyback proponents will point out that many Americans own stock and therefore benefit from buybacks. That’s true, but rich Americans own the most. According to Gallup , just over half of Americans own stocks at all. The richest 10 percent of Americans own 80 percent of all stock shares, while the bottom 80 percent of earners own just 8 percent.

Executives and corporate insiders are major also beneficiaries of buybacks, because they take advantage of them to sell shares they’re rewarded as part of their compensation.

Politico reported that a recent review of SEC filings shows that executives, who often receive much of their compensation in the form of stock, have been selling many of their shares since the tax bill was passed, just as buyback activity is on the rise. Eastman Chemical CEO Mark Costa sold $5.4 million worth of shares two days after the company announced a $2 billion repurchase. Mastercard CEO Ajay Banga sold $44.4 million of stock — the largest sale by an executive from the company over the past decade — months after it announced a $4 billion buyback.

Corporate executives have to disclose share purchases or sales within two days of the transaction.

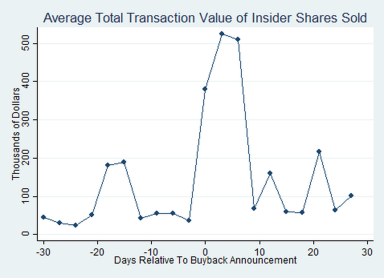

Jackson, the SEC commissioner, earlier this year unveiled research showing how common it is for executives to use buybacks to cash out of their stock holdings. His team looked at 385 buybacks since the start of 2017 and found that in half of them, at least one executive sold shares in the month following the buyback announcement. Twice as many companies had insiders selling in the eight days after a buyback announcement as they would on any other normal day.

The thing is that it’s perfectly legal for all of this to happen. The SEC rule governing stock buybacks doesn’t bar executives from selling shares during a buyback. In fact, that rule hasn’t been touched since 2003 , when the SEC required companies to disclose more information on share repurchases, among other amendments. The change made companies disclose a little more information and a little more often, but they still don’t have to say exactly when buybacks are taking place or who is selling shares during them.

In 2015, then-SEC Chair Mary Jo White acknowledged in a letter to Sen. Tammy Baldwin (D-WI), who has taken interest in the buyback issue, that the agency doesn’t collect data that would let it know whether companies are actually in compliance with SEC buyback rules.

“I call it the looting of the US industrial corporation,” Lazonick said. “It’s legal, and it’s totally unregulated.”

Jackson, who was confirmed as an SEC commissioner in December 2017 alongside Republican Hester Peirce, gave a more measured assessment but acknowledged that the fact that the SEC hasn’t revisited buyback guidelines in 15 years is a real problem.

There are proposals out there on curbing stock buybacks, but it’s not clear how far they’ll go

Baldwin has taken a keen interest in looking at stock buybacks from Capitol Hill. She wrote letters to former SEC Chair White and current Chair Jay Clayton asking them to take a look at buyback rules. Clayton has not replied to the latest letter, Baldwin’s office said. She put a temporary hold on Jackson and Pierce’s SEC nominations, asking them to respond to her questions about buybacks and short-termism, which they did.

In March, Baldwin introduced the Reward Work Act . The legislation would make stock buybacks more transparent by requiring they be conducted through tender offers, which are subject to more disclosure. It would also require one-third of corporate board members to be elected by workers. Sens. Elizabeth Warren (D-MA), Brian Schatz (D-HI), and Kirsten Gillibrand (D-NY) have signed on as cosponsors of the bill, and Rep. Keith Ellison (D-MN) has introduced it in the House .

Baldwin, in an interview, discussed what drove her interest in buybacks. “There were a series of things that I had heard about that concerned me — of a decreasing commitment in publicly traded companies and others to raising wages, to investing in modernizing equipment, to worker training as they were becoming more advanced,” she said. “And I thought, ‘Why is this? Why is this trend going in a direction that we wouldn’t want to see, especially when these companies are really quite profitable?’”

Baldwin in June sent a letter to Wells Fargo CEO Tim Sloan asking about the company’s announcement it would close a call center in Menomonee Falls, Wisconsin, laying off the 46 employees who worked there, months after the bank got a major tax cut and said it would spend $22 billion on stock buybacks.

“Every community can see examples of this in their own backyard,” Baldwin said. “Whether it’s drug companies that have engaged in stock buybacks after their windfall in the tax bill instead of lowering the price of life-saving prescription drugs or life-extending prescription drugs, or you can see companies closing factories that they make the choice to do hundreds of millions of dollars in stock buybacks.”

Sens. Cory Booker (D-NJ) and Bob Casey (D-PA) in March also introduced legislation, the Worker Dividend Act , that would require companies buying their own shares to pay out to their own employees, too. Booker told Vox’s Matt Yglesias that he sees the bill as a “commonsense move to address a variety of ills.”

Many other developed countries are more restrictive of stock buybacks . For example, in Japan, the UK, France, Canada, the Netherlands, Hong Kong, and Switzerland, there are explicit restrictions and disclosure requirements for executives who trade during buybacks. All Swiss buyback transactions are fully disclosed. Japan, the UK, the Netherlands, and Hong Kong require share buyback executions to be reported immediately or within a day of when they happen.

In the US, it’s not clear what chance, if any, the laws and rules around buybacks have of changing. In Republican-controlled Congress, Baldwin’s and Booker’s bills are unlikely to go anywhere. Commissioner Jackson is pushing for the SEC to revisit buyback rules, but he’s one of five commissioners, and it’s not clear whether there’s the sufficient appetite among the others to do it.

There’s increasing attention being paid to stock buybacks, especially in light of the tax cuts, and that could pressure lawmakers and regulators to do something — say, stop executives from being big beneficiaries of the practice. “That’s exactly the kind of thing that convinces Americans to think our markets are rigged,” Jackson said.

Tags

Who is online

55 visitors

So it turns out that the tax-cut for corporations has turned out, in fact, to be just another way of funneling money to the already-rich.

Gosh.

That's a surprise....