Christine Lagarde will have to confront Berlin if she’s to save the euro

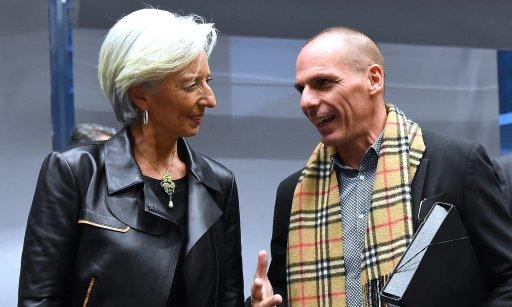

‘She even acknowledged that Greece had been given a raw deal.’ Christine Lagarde, then IMF director, and Yanis Varoufakis, then Greece’s finance minister, in 2015.

Emmanuel Dunand/AFP/Getty Images

The other key figure alongside the International Monetary Fund’s then managing director was Mario Draghi, president of the European Central Bank, who played a central role in that drama by engineering the closure of Greece’s banks . Now, four years later, Lagarde has been anointed to succeed Draghi at the helm of the ECB.

Despite her role, and the dealings we had when I was Greece’s finance minister, not once did I feel animosity towards her. I found her intelligent, cordial, respectful. She even acknowledged, in private at least, that Greece had been given a raw deal and that my campaign to cut our public debt was right and proper. Lagarde’s priority was holding the troika’s line and minimising any challenge to its collective authority.

The question now is whether Lagarde’s skills are in tune with the task of leading the ECB in the post-Draghi era. Much has been made, by supporters and detractors, of both her unquestionable talent for managing complex institutional tensions and her non-existent monetary policy background. Perhaps it is not a coincidence that the two most influential central banks, the Federal Reserve and the ECB, are now to be led by lawyers with no academic monetary background. The shifting consensus on who is best placed to oversee monetary policy reflects a crisis of financialised capitalism that traditional central banking can no longer address.

Lagarde’s greatest challenge is that she is replacing a man credited with saving the eurozone by means of policies that are no longer fit for purpose. If she departs from Draghi’s script, she will face fierce criticism. And if she does not, the eurozone’s never-ending crisis will spin further out of the ECB’s control.

Draghi saved the eurozone by printing trillions of euros to fund the bankrupt banks and to allow Italy, Spain and other stressed states (though not Greece) to roll over their debts. To do this, he needed to skilfully subvert the eurozone’s rules which, in turn, required painstaking work to co-opt Germany’s Angela Merkel in his great clash with both the Bundesbank, Germany’s powerful central bank, and Wolfgang Schäuble , Germany’s finance minister.

While Draghi’s wall of money helped the eurozone perk up, it could not cure its underlying disease and had some pretty nasty side-effects. Stubborn negative interest rates continue to undermine pension funds and insurance companies in Germany and beyond. Rates remain negative because investment is woefully low due to investors’ self-fulfilling pessimism given the prospect of more austerity.

This creates deflationary pressures that eat into the savings of the middle class, replace quality jobs with precarious ones and, thus, beget political monsters across Europe .

Most commentators wonder whether Lagarde will be brave enough to continue with Draghi’s “unconventional” policies. This is the wrong question to ask since his trick for keeping key countries, such as Italy, in the eurozone has reached the end of the road both technically and politically.

Technically, because Draghi’s success in persuading Berlin to let him buy Italian public debt, and thus keep Italy in the eurozone, hinged on the promise to buy debt from each member state in proportion to the size of their economy – ie buying approximately €2 of German debt for every €1 of Italian debt. However, with Germany producing no new public debt, courtesy of running a budget surplus, Draghi’s strategy for buying Italian debt has fizzled out.

And politically, Draghi’s trick has also expired because the deflationary dynamic of the last decade has given birth to a Eurosceptic rightwing Italian government unfazed by the prospect of Italy dropping out of the eurozone.

The pertinent question to ask about Lagarde’s ECB tenure is: can she push Berlin to ditch the eurozone’s suicidal fiscal rules (which reinforce Europe’s deflationary dynamic) and to accept the idea of a common, safe debt? If she does not do so, no matter how energetically she continues to impose Draghi’s policies, she will fail the test of history. To succeed she needs to be subtle, creative and confrontational.

Subtlety requires that she does not ask Berlin explicitly to denounce dogmas that have, over the years, acquired quasi-religious status.

Creativity will help her sell the abandonment of fiscal rules as their reinforcement, via the interest rate mechanism. For example, Lagarde could propose that the ECB help member states refinance their debt, but only the part they were allowed to have according to the eurozone’s own rules – thus, giving Rome a market-based disincentive to borrow excessively. Similarly, there are imaginative ways to create the common debt that Berlin detests but which is essential to the smooth operation of any monetary union – for example, by insisting that the ECB borrows on its own account to roll over Italian, Spanish, German, etc, debt already purchased under Draghi.

Lagarde is certainly smart enough to grasp the necessity of such a feat – and to pull it off if she puts her mind to it. The real question is whether she has the inclination to confront Berlin head-on, to the point of telling the German government that it is her way or, ultimately, the end of the euro and a chaotic return to the deutschmark. The omens, I am afraid, are not good.

During her IMF days in Washington, Lagarde often had to choose between policies that were to Berlin’s liking or in the fund’s interests. The clearest example was over the extending of Greece’s insolvency by a lethal combination of more loans and more income-sapping austerity. While the IMF’s staff were adamant that Greece needed an outright debt reduction, Lagarde repeatedly sided with Berlin. Forced to choose between Berlin’s favouritism and the interests of the institution she led, she unfailingly opted for the former. If she continues this behaviour after her Frankfurt move, her ECB career will prove inauspicious.

Yanis Varoufakis is the co-founder of DiEM25 (Democracy in Europe Movement). He is a former finance minister of Greece

Tags

Who is online

74 visitors

People have been predicting doom for the euro since day one. My main guy Paul Krugman is among the many, many who have been wrong on this. As always, Krugman eventually could not ignor the fact that his doomsaying was... wrong. As always, he re-examined his thinking, to see where he has gone wrong. He concluded that he had not understood the depth of the political/diplomatic aspects of the euro. He has been much more circumspect, since then.

So here we have Varoufakis predicting doom. Once again, his technical analysis is probably correct. But politics.....

Personally, I'd like to see Lagarde follow Varoufakis's line... but then there's Germany........